There has been a significant increase in Apple (AAPL) rumors and speculation regarding earnings from both the analyst community and in Seeking Alpha as we run up to their July 24th earnings report.

Apple Inc., together with subsidiaries, designs, manufactures, and markets mobile communication and media devices, personal computers, and portable digital music players; and sells related software, services, peripherals, networking solutions, and third-party digital content and applications worldwide. Its products and services include iPhone, iPad, Mac, iPod, Apple TV, the iOS and Mac OS X operating systems, iCloud, and various accessory and support offerings, as well as a range of consumer and professional software applications

There were some telling trends in the recent Intel (INTC) conference call. Most notable was the company's calm regarding the Europe slowdown and its control of expenses to meet margin targets. Although I don't see any profound read through from the Intel report, its demeanor and comments on both pipeline and inventory build with regard to the Microsoft (MSFT) Windows 8 launch do provide some visibility to the competitive landscape for the remainder of 2012. A notable comment was the number of variations on the Windows 8 tablet design. Intel referenced 40 different tablet designs and made continued comments about the Ultrabook market. It also claimed that consumers in this rocky economic climate tended to buy higher quality and higher priced devices. This is good for Apple. These comments do not alter my commitment to Apple and its sales possibilities but do tame my enthusiasm for another parabolic price run following earnings. This tempering is due to macro economic events not Apple-specific activity.

Emotion can cause havoc with regard to investing and Apple is an emotion-influenced company. I treat Apple consumer emotion as a form of good will that translates to trend-breaking sales. The company's recent stock run up has been the poster boy for success in the market. Consumer emotion in the case of Apple is a positive for sales as consumers have proven willing and able to continue to purchase higher priced devices even though competitors have improved. I view this as a critical attribute in emerging markets including China. Even in the face of increased, higher quality competition unit sales increase due in part to goodwill.

In anticipation of the earnings report, I have tempered my expectations but remain positive on Apple long term. To take advantage of this I have adjusted my trading thesis. I remain long Apple. It is not a company I would reduce exposure to for the remainder of 2012. With the anticipated product refresh cycle and new product introductions, there remains significant upside potential. I do not anticipate the wild swings in pricing seen in past quarters following the quarterly report. This belief is due in part to the product refresh cycle not taking hold until October.

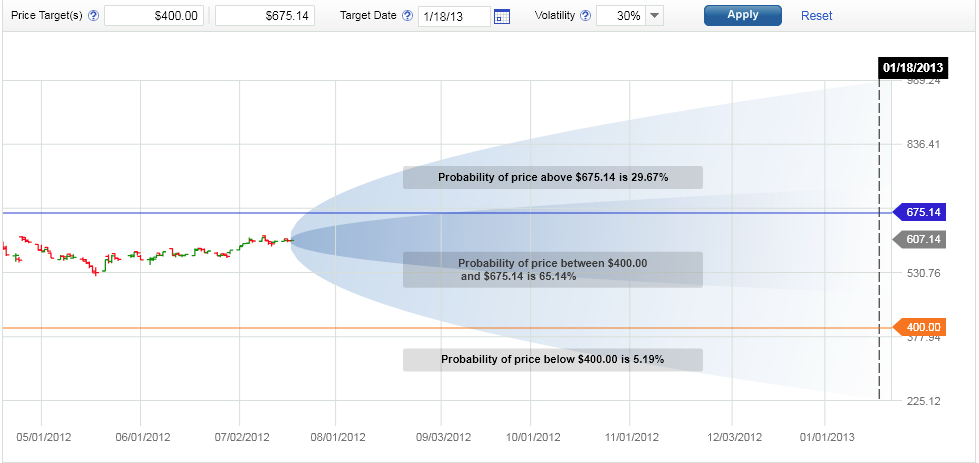

To take advantage of timing for the remainder of 2012 I have added deep in-the-money calls to my holdings starting with a January 2013 expiration. Hopefully this will give me enough room for the transitory news to percolate through the share price. The first leg in my adjusted tactical plan is a 500 strike call purchased last week. I plan to hold this through earnings and add to the holding if the share prices falls below $600. For this strategy I am targeting an end of 2012 breakeven price of $622 with $644 as the high range. The chart below outlines pricing probability for the price ranges $400 to $675.

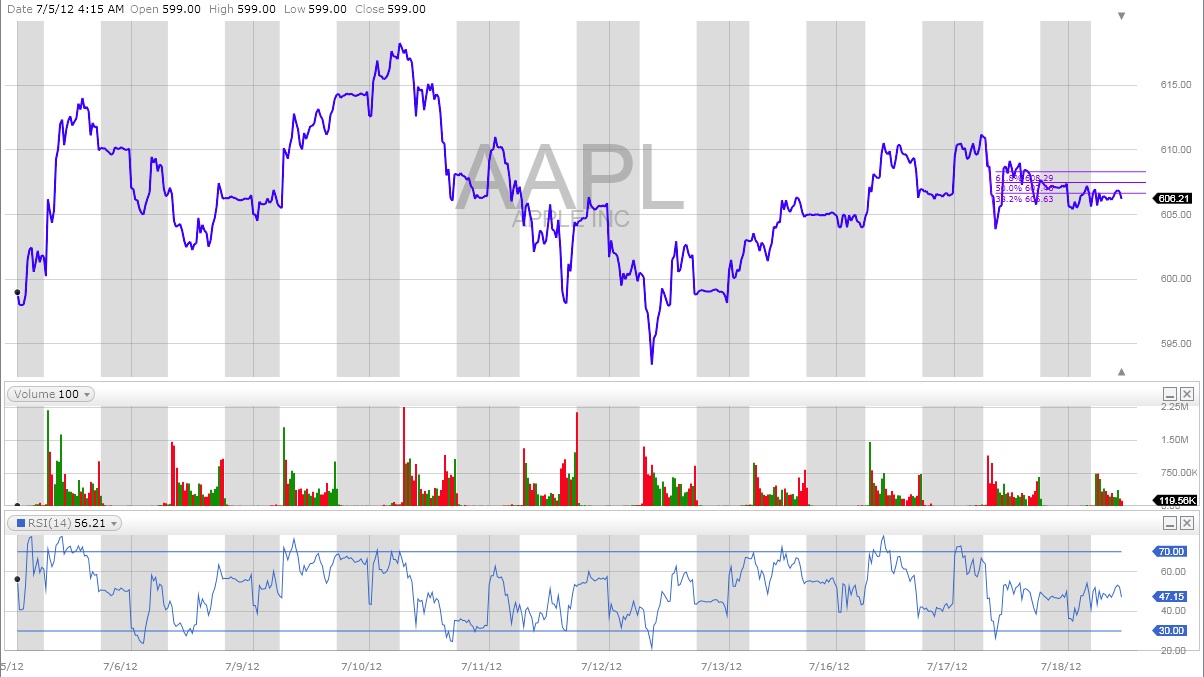

I will add a lower strike call to my mix if share prices drop on earnings targeting a $450 strike which is trading today at $157.20. In the past I have used covered calls but have elected to not put any long shares at risk. I targeted the $450 Call attempting to both lower my break even costs if I elect to buy shares in January as well as the higher volume at this strike price. With over 4000 open interest orders and volume of 305 it has the trading exposure needed. Although I am not a technical trader there is an interesting trend developing represented in the chart below.

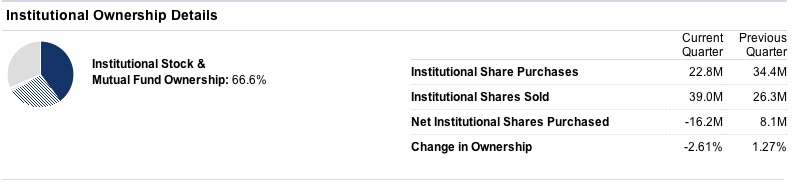

Each day has opened with a volume spike. I attribute this to machine trades as I have not been able to correlate the activity to news or company announcements. I mention this perceived trend because of the downdraft in share pricing last quarter. Mainstream media pronounced with their usual zeal that this was because Apple was acting as a bank for hedge and mutual funds struggling to meet their profit targets. With the RSI near a mid point of 59.60 and more shares sold by institutions this quarter than last it appears that fund managers are staging for a downturn.

If there is a downturn I will add to my deep in the money call positions and remain long Apple.

Tactical Plan:

- Long Apple shares

- Call with a January 2013 expiration at $500

- Cash Secured Put Strike $275 January 2013 expiration

- Add January 2013 Strike $450 if the price declines.

If I am wrong and there is a ground breaking quarter I can sell the call and bank the profits to reinvest on the next downturn. My price target to consider trading out of the Call is $640.

No comments:

Post a Comment